{kind=link}

Picking the cheapest car insurance quote first is the fastest way to a nasty surprise.

Without a plan you can miss coverage gaps, hidden fees, and weak claims service.

This checklist shows exactly what to collect and compare: premiums, limits, deductibles, discounts, insurer ratings, and exclusions so you can make an apples-to-apples choice.

Follow it and you’ll spot real value fast, not just the lowest sticker price, and start by locking in the same limits and deductibles before you shop.

Core Checklist for Comparing Car Insurance Quotes Effectively

A structured checklist stops you from choosing car insurance based on price alone. When you compare quotes without a plan, you risk missing coverage gaps, surprise fees, and weak claims performance. A good checklist captures premiums, coverages, limits, deductibles, insurer reliability, and policy terms in one place so you can see exactly what you’re buying and what you’re giving up.

To ensure apples-to-apples evaluation across insurers, every quote you collect needs identical coverage limits, the same deductible amounts, and the same drivers and vehicles. If one quote assumes a $500 collision deductible and another uses $1,000, the premium difference reflects the deductible gap, not insurer pricing. Lock in your coverage decisions before you shop, then fill in the same checklist fields for each quote you receive.

Before you decide, your checklist must capture financial strength ratings, claims satisfaction scores, and policy exclusions. You need to know if the insurer will still be solvent in five years, how long claims take to settle, and whether your rideshare side gig or custom stereo install voids coverage.

Essential checklist fields for each quote:

- Insurer name

- Annual premium and monthly premium (including installment fees)

- Liability limits (bodily injury per person / per accident / property damage)

- Uninsured/underinsured motorist limits

- Collision deductible and comprehensive deductible

- Rental reimbursement (dollars per day and total maximum, for example $30 per day up to $900)

- Towing and roadside assistance limit (for example $50 to $200 per incident)

- Discounts applied (list each discount type and percentage)

- AM Best financial strength rating (target A‑ or better)

- Claims satisfaction data (J.D. Power ranking or NAIC complaint ratio)

- Average claim response time (initial contact within 24 to 72 hours; payout 3 to 14 days)

- Cancellation policy and grace period (typically 10 to 30 days)

- Policy exclusions and special endorsements

Information Required Before You Start a Car Insurance Quote Comparison

You can’t get accurate quotes without accurate inputs. Gather your VIN, vehicle year, make, model, and current odometer reading before you contact any insurer. VIN accuracy prevents mismatched rates because insurers pull repair cost data, safety scores, and theft risk tied to your exact trim level. Garaging ZIP code affects your rate more than almost any other factor. If you live in one ZIP and garage the car in another, use the garage location.

You also need driver license numbers for every household member who’ll be listed or excluded on the policy, annual mileage (your best honest estimate), and a complete driving history for the past three to seven years. That means dates and details for every accident, claim, and moving violation. Pull your current or most recent policy declarations page so you can reference the limits and coverages you already have.

Documents and details to collect before requesting quotes:

- Vehicle Identification Number (VIN)

- Current odometer reading and expected annual mileage

- Driver’s license numbers for all drivers in the household

- Driving record for the past three to seven years (accidents, violations, claims)

- Garaging address and ZIP code

- Current policy declarations page (if you have one)

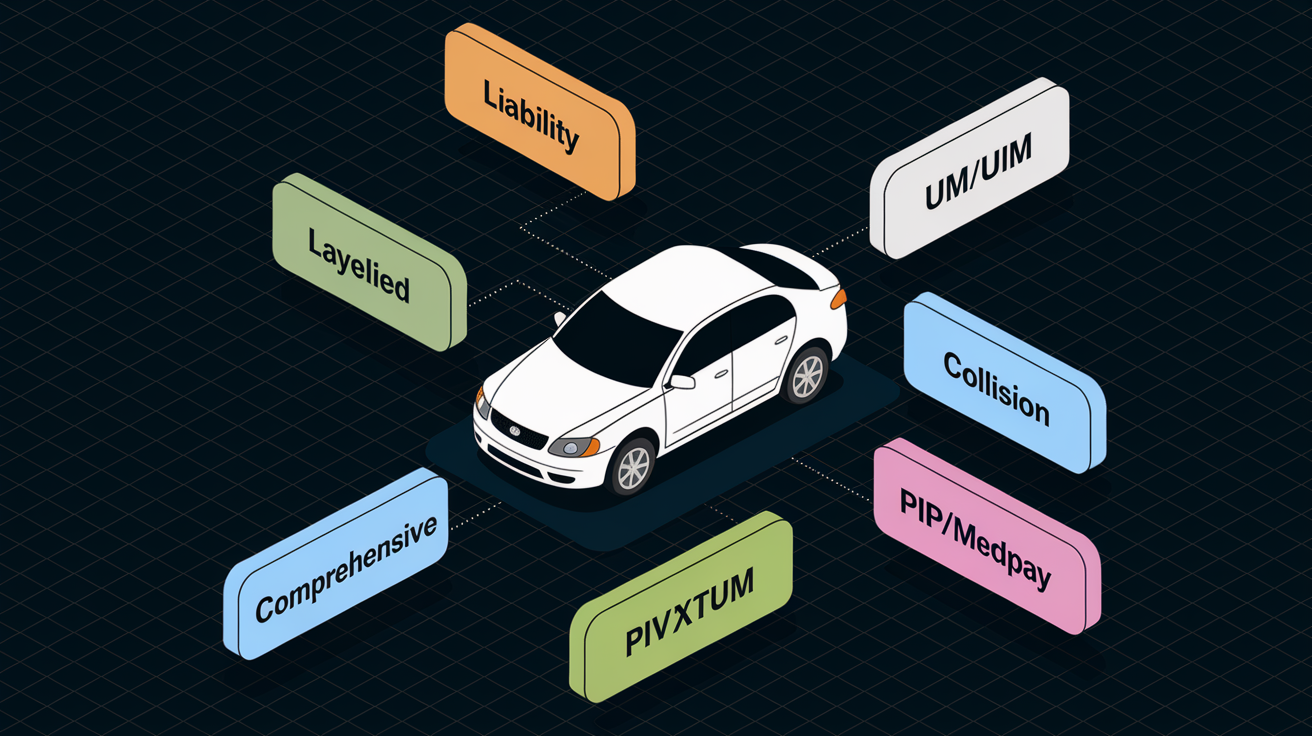

Coverage Comparison Checklist for Car Insurance Quote Evaluations

Your coverage checklist is where most hidden gaps live. Every quote needs to break out the same coverage types so you can compare what you’re actually buying.

Required and Optional Coverage Types

Liability coverage is mandatory in almost every state. State minimum examples often look like 25/50/20, which means $25,000 bodily injury coverage per person, $50,000 per accident, and $20,000 property damage per accident. Financial advisors and consumer advocates recommend a baseline of 100/300/100 or higher to protect your assets if you cause a serious crash.

Uninsured and underinsured motorist coverage (UM/UIM) protects you when the other driver has no insurance or not enough. Match your UM/UIM limits to your liability limits whenever your state allows it. Collision covers damage to your car in a crash, regardless of fault. Comprehensive covers non-crash losses like theft, vandalism, hail, or hitting a deer. Personal Injury Protection (PIP) or Medical Payments (MedPay) cover medical bills for you and your passengers, no matter who caused the accident. PIP is mandatory in no-fault states; MedPay is optional elsewhere.

Coverage Limits and Deductible Strategy

Collision and comprehensive deductibles typically range from $250 to $1,000. Choosing a $1,000 deductible instead of $500 often cuts your collision premium by 10 to 30 percent, but you pay an extra $500 out of pocket if you file a claim. If your car’s worth $3,500 and your collision deductible is $1,000, the math gets tight. A total loss pays you roughly $2,500 after the deductible, so some drivers drop collision on older vehicles to save money.

Liability limits protect your income and assets. If you cause an accident that injures multiple people, a 25/50 bodily injury limit might cover the first victim’s hospital bill and leave the rest uncovered. Higher limits cost more per month but far less than a lawsuit.

Extra Add-ons to Compare

Rental reimbursement pays for a rental car while yours is in the shop after a covered claim. Typical limits are $20 to $50 per day, with a total maximum of $600 to $1,500. Towing and labor coverage runs $50 to $200 per incident or per year, depending on the insurer. Roadside assistance bundles towing, jump-starts, lockout service, and flat-tire help. Gap insurance pays the difference between what you owe on your loan and what the car’s worth if it’s totaled. OEM parts endorsements guarantee original manufacturer parts instead of aftermarket replacements during repairs.

Coverages that often differ between insurers:

- Rental reimbursement daily limits and total maximums

- Towing and labor caps (per incident vs. annual aggregate)

- Glass deductible waivers (some states require zero-deductible windshield replacement)

- Rideshare or delivery driver endorsements

- Custom equipment coverage for aftermarket stereos, lifts, or wheels

- New-car replacement or loan/lease gap coverage

Premium, Fees, and Discount Comparison Checklist

Premiums look simple until you compare monthly versus annual totals. An insurer quoting $100 per month might charge $1,200 annually if you pay in full, or $1,230 if you pay monthly because of a $10 to $30 installment fee each month. Always record both the annual premium and the true monthly cost including fees.

Quote spreads between insurers commonly run 20 to 40 percent even when coverage is identical, so collect at least three quotes. Discounts shrink that gap, but only if they’re applied correctly. Ask every insurer to itemize which discounts you qualify for and how much each one saves. Some companies advertise discounts but fail to apply them unless you ask.

| Discount Type | Typical Range |

|---|---|

| Multi-policy (home + auto) | 10–25% |

| Multi-car | 5–20% |

| Safe driver / accident-free | 10–30% |

| Good student | 5–25% |

| Anti-theft / safety equipment | 5–15% |

| Pay-in-full / annual pay | 5–15% |

Car Insurance Quote Comparison Table: How to Build a Side-by-Side Matrix

A spreadsheet or simple table format keeps all your quotes visible in one view. Set up columns for each quote and rows for each comparison metric so you can scan across and spot differences instantly. Start with price, then add coverage details, then insurer quality markers, then policy terms.

Use a weighted scoring method if you want a numeric comparison. Assign weights like this: price 40 percent, claims service 25 percent, financial strength 15 percent, coverage extras 10 percent, policy terms 10 percent. Multiply each insurer’s score in each category by the weight, add them up, and the highest total wins. You can also calculate a three-year cost projection by multiplying the annual premium by three and adding one likely deductible for a realistic scenario.

Recommended columns for your side-by-side comparison table:

- Insurer name

- Policy effective date and quote expiration date

- Annual premium and monthly premium (with fees)

- Liability limits (bodily injury per person / per accident / property damage)

- Uninsured/underinsured motorist limits

- Collision deductible and comprehensive deductible

- Rental reimbursement (per day and total max)

- Towing and roadside limit

- Discounts applied (itemized with dollar or percentage amounts)

- AM Best rating or equivalent financial strength score

- J.D. Power ranking, NAIC complaint ratio, or customer satisfaction note

- Claim response time estimate and average payout timeline

- Cancellation policy, grace period, and renewal terms

- Exclusions, endorsements, and coverage notes

Evaluating Insurer Reliability During a Car Insurance Quote Comparison

Financial strength matters because an insurer that goes bankrupt can’t pay your claim. Check the AM Best rating for every carrier on your list and aim for A‑ or better. Anything below that suggests higher financial risk. You can find AM Best ratings on the insurer’s website, on rating agency sites, or through your state insurance department.

Claims satisfaction tells you how the company treats you after an accident. Use J.D. Power rankings for auto claims satisfaction, or check the National Association of Insurance Commissioners complaint index to see how many complaints each insurer receives relative to its size. Look for carriers in the top half of satisfaction rankings and the bottom half of complaint ratios. Ask how long initial claim contact takes, whether a local adjuster will inspect your car, and what the average payout timeline looks like. Benchmarks to expect: initial response within 24 to 72 hours and payout resolution in 3 to 14 business days for simple claims.

Customer service quality shows up in how easy it is to reach someone, change your policy, or get answers. Read recent online reviews, but focus on patterns, not one-off complaints. If multiple reviews mention delayed claim checks or unhelpful agents, that’s a red flag. If most praise fast service and fair settlements, that’s a green light.

Fine‑Print Review Checklist for Car Insurance Quote Comparison

Policy exclusions live in the fine print and can void coverage when you need it most. Common exclusions include using your car for rideshare or delivery without the proper endorsement, commercial use, intentional damage, racing, and driving under the influence. Some insurers exclude coverage for aftermarket modifications unless you buy a custom equipment endorsement.

Cancellation rules and grace periods vary by insurer and state. Most companies give you a 10 to 30 day grace period if you miss a payment, but some cancel immediately after the grace period ends and charge a short-rate penalty if you cancel mid-term. Nonrenewal notices tell you how much warning you’ll get if the insurer decides not to renew your policy, which matters if you need time to shop for replacement coverage without a lapse.

Fine-print items to verify on every quote:

- Exclusions for rideshare, delivery, or commercial use

- Cancellation and nonrenewal notice periods

- Grace period length for missed payments

- Different deductibles for collision versus comprehensive (some policies list them separately)

- Sub-limits on rental reimbursement, towing, or custom parts

- Endorsements that change standard coverage (for example, named-driver exclusions or mileage caps)

Timing, Switching Steps, and Post‑Quote Checklist

Re-shop your car insurance every 6 to 12 months, or immediately after a life change like a move, new car purchase, marriage, adding a teen driver, or receiving a ticket. Rates shift constantly, and loyalty doesn’t pay. Insurers raise renewal premiums knowing most customers won’t compare quotes, so treat every renewal like a new shopping cycle.

When you’re ready to switch, coordinate effective dates to avoid coverage gaps or overlaps. A lapse in coverage, even one day, can trigger rate increases that last three to five years and may violate state financial responsibility laws. Request your new policy to start the day after your old one ends. Get written confirmation of the new effective date and a binder or policy number before you cancel the old policy.

Steps for switching car insurance safely:

- Choose your new insurer and finalize coverage details, limits, and discounts.

- Confirm the effective date and get a binder or policy confirmation in writing.

- Contact your current insurer and request cancellation effective the day before the new policy starts.

- Ask for a refund calculation if you’ve prepaid; confirm the final cancellation date in writing.

- Keep proof of continuous coverage (declarations pages from both policies) for at least three years in case of disputes or audits.

Final Words

Start by gathering the facts—VIN, mileage, driver history, and your current declarations page—then record each quote using the core checklist fields like premiums, liability, deductibles, UM/UIM, rental, towing, and discounts.

Next, build a simple side-by-side matrix, check insurer ratings and claims timing, and read the fine print for exclusions, grace periods, and fees.

Follow this car insurance quote comparison checklist and you’ll pick the best mix of price and protection with less stress and more confidence.

FAQ

Q: What is the best and most reliable site to compare car insurance quotes?

A: The best and most reliable way to compare car insurance quotes is to use 2+ aggregator sites (for example, NerdWallet or The Zebra) and also check insurer websites; verify AM Best and J.D. Power ratings before choosing.

Q: What not to tell your insurance company?

A: You should not tell your insurance company that you’re definitely at fault, give speculative details, agree to an on-record statement without advice, post about the crash online, or hide commercial/ride-share use of your car.

Q: Who typically has the cheapest car insurance?

A: Drivers who typically have the cheapest car insurance are older, experienced drivers with clean records, low annual mileage, higher deductibles, good credit where allowed, and vehicles with strong safety and low theft rates.