{kind=link}

What if the person who hit you drove away—are you stuck paying the bills?

If you have uninsured motorist (UM) coverage, it can pay for injuries and, in some states, car damage when the other driver is unknown.

This post shows step-by-step what to do at the scene, which documents matter, the common deadlines that trip people up, and how to work with an adjuster so your UM hit and run claim has the best chance of success.

Immediate Actions After a Hit‑and‑Run

The first minutes after a hit and run decide whether your uninsured motorist claim goes through or gets tangled in disputes. Your insurer wants proof the crash happened and that the other driver took off. The faster you move, the better your claim looks.

Here’s what to do right away:

-

Stop somewhere safe. Pull to the shoulder, a parking lot, or the nearest spot where you’re not blocking traffic. Hazards on.

-

Call 911 and report the hit and run. Tell the dispatcher the other vehicle left. Most UM claims need a police report within 24 to 72 hours. If you can, note the vehicle’s make, color, direction, or even a partial plate.

-

Use your phone to document the scene. Photos of vehicle damage, skid marks, debris, your location, traffic signals, street signs. Capture time and date. If someone stopped to help, photograph where their vehicle is.

-

Get witness information. Names, phone numbers, a quick statement from anyone who saw the crash or the car driving away. Witnesses back up your story and confirm the incident actually happened.

-

Write down what you remember. While it’s fresh, record what went down: time, direction of travel, weather, where the other car hit you, what you saw before impact. Memory gets fuzzy fast.

-

Get medical care now. Even if you feel okay, adrenaline hides injuries. See a doctor the same day or within 24 hours. Waiting gives insurers a reason to question whether the crash really hurt you.

-

Call your insurer within hours. Same day. Tell them the other driver is uninsured or unknown and that you’re filing a UM claim. Give them the police report number, photos, and witness details once you’ve got them.

Most insurers want notice “immediately” or “as soon as practicable.” Usually that’s 24 to 48 hours. Late reporting is the top reason UM hit and run claims get denied. Your policy might have a specific deadline. If you wait days or weeks without a solid reason (like being in the hospital), your insurer can refuse to pay. Report the crash even if you’re still collecting evidence. You can send documents later.

State‑Specific Reporting Requirements and Deadlines

Every state has its own rules for when and how you report a hit and run. Miss a deadline and your UM claim can shut down before you even file. Most states want immediate police notification, and many insurers won’t touch a UM hit and run claim without an official police report filed within 24 to 72 hours.

Some states also want a written statement to your insurer within a set window, often 30 days from the crash. Check your policy declarations page or call your insurer to confirm what your state requires. If your state says written notice and you miss the cutoff, the insurer might deny your claim outright, even if you reported the crash verbally.

Here’s what states commonly require:

- Immediate police report. Most states treat a police report filed within 24 to 72 hours as “immediate.” Longer delays need documented reasons (hospitalization, serious injury).

- Written statement to insurer. Some policies want a signed, written account of the crash within 30 days. Verbal notice alone might not count.

- Physical contact rule. A few states need proof that the hit and run vehicle actually made contact with your car or body. If the other driver forced you off the road without touching your vehicle, UM might not apply.

- DMV notice. Certain states want a separate accident report filed with the Department of Motor Vehicles, especially if damage goes over a dollar threshold (say, 1,000 dollars or 1,500 dollars).

- Cooperation clause. Almost every policy says you have to cooperate with the insurer’s investigation. Refuse to give a recorded statement or refuse a vehicle inspection and your claim can disappear.

If you’re not sure what your state needs, call your insurer’s claims line the day of the crash. Ask, “What are my reporting deadlines for a UM hit and run claim?” Write down the representative’s name, date, time, and what they said.

How Uninsured Motorist Coverage Applies to Hit‑and‑Run Accidents

Uninsured motorist coverage (UM) pays for injuries and, in some states, property damage when the at fault driver has no insurance or can’t be identified. A hit and run counts as an “uninsured driver” because you can’t collect from someone you can’t find. Your own UM coverage steps in as if the fleeing driver had been insured under your policy.

UM coverage usually has two parts. Uninsured Motorist Bodily Injury (UMBI) covers medical bills, lost wages, pain and suffering, and future care costs. Uninsured Motorist Property Damage (UMPD) covers vehicle repair or replacement, but not all states offer UMPD, and some cap it at a low limit (say, 3,500 dollars). Check your declarations page to see what you carry.

One big rule in many states: the hit and run vehicle must have made physical contact with your car or body. If another driver forced you into a ditch but never touched your vehicle, UM might not apply. Some states waive the physical contact rule if you have independent witnesses who saw the other vehicle cause the crash. If you’re a pedestrian or cyclist struck by a hit and run driver, UM usually applies. Check your policy language to confirm coverage for non-occupants.

The three main UM pieces in hit and run situations:

- UMBI for injuries (medical costs, lost income, pain and suffering).

- UMPD for vehicle damage (if your state allows it and your policy includes it).

- Physical contact requirement in certain states. Independent witnesses or video can sometimes substitute if no contact happened.

If you only carry collision coverage, you can still file for vehicle damage under collision, minus your deductible. But collision won’t cover your injuries. UM is the only coverage that pays for both injuries and, in some cases, property damage when the at fault driver is unknown.

Required Documentation for a Strong UM Claim

Insurers handle UM hit and run claims only when you prove the crash happened and the other driver left. Consistent, detailed documentation turns a weak story into a credible claim. Gather these documents as soon as possible and send them to your insurer in one organized package.

Start with the police report. Your insurer will want the report number, the responding officer’s name, and the department contact. If the report’s not ready yet, follow up with the police department weekly until it’s available. The report shows the crash was officially recorded and that you reported it quickly.

Next, pull together medical records and itemized bills from every provider: emergency room, follow up doctors, physical therapy, prescriptions, and any imaging (X-rays, MRIs). Keep a separate folder for each type of record. If you haven’t seen a doctor yet, go today. Waiting a week makes insurers question whether the crash caused your injuries.

- Police report (report number, officer contact, incident details).

- Medical records and bills (ER visit, follow ups, therapy, medications, diagnostic tests).

- Photos and videos (vehicle damage, scene, injuries, skid marks, debris, date/time stamps).

- Witness statements (names, phone numbers, written or recorded accounts).

- Repair estimates (at least two estimates if your vehicle is drivable; total loss appraisal if it’s not).

- Proof of lost wages (pay stubs, employer letter, tax returns if self employed).

If you kept a daily journal of pain, missed activities, or emotional effects, include that too. A sentence each day (“Couldn’t pick up my daughter because my back locked up”) adds human detail insurers can’t brush off. Save receipts for every out of pocket cost: Uber to doctor appointments, over the counter pain relievers, rental car while yours is in the shop. Small costs add up and belong in your claim.

How Insurers Investigate Hit‑and‑Run UM Claims

Your insurer’s job is to confirm the hit and run happened, that the other driver is truly unknown or uninsured, and that your damages match the crash. The investigation starts the moment you report the claim. An adjuster will review the police report, compare your statement to physical evidence, and look for consistency across all your documents.

Expect the adjuster to request a recorded statement within a few days. They’ll ask where you were going, what you saw, how the crash happened, and when you first felt pain or noticed damage. Answer honestly and keep it simple. If you don’t remember a detail, say “I don’t remember” instead of making something up. Inconsistencies between your recorded statement and the police report throw up red flags.

The adjuster might also inspect your vehicle in person or ask for photos from multiple angles. They’re checking whether the damage lines up with your description of the crash. Rear end impact should show rear end damage, not side swipe marks.

If you listed witnesses, the insurer will contact them to verify your account. They might also check nearby businesses for surveillance footage or request traffic camera records from local authorities. If the insurer finds video showing the other vehicle or confirming your version, your claim becomes much harder to dispute. If no independent evidence exists, the claim relies on your credibility and the consistency of your records.

The investigation can take a few weeks to a few months, depending on complexity. During this time, keep submitting updated medical bills and records as treatment continues. If the adjuster goes silent for more than two weeks, call and ask for a status update. Document every conversation: date, time, representative name, claim number, and what was discussed. That log becomes critical if the insurer later denies your claim or delays payment.

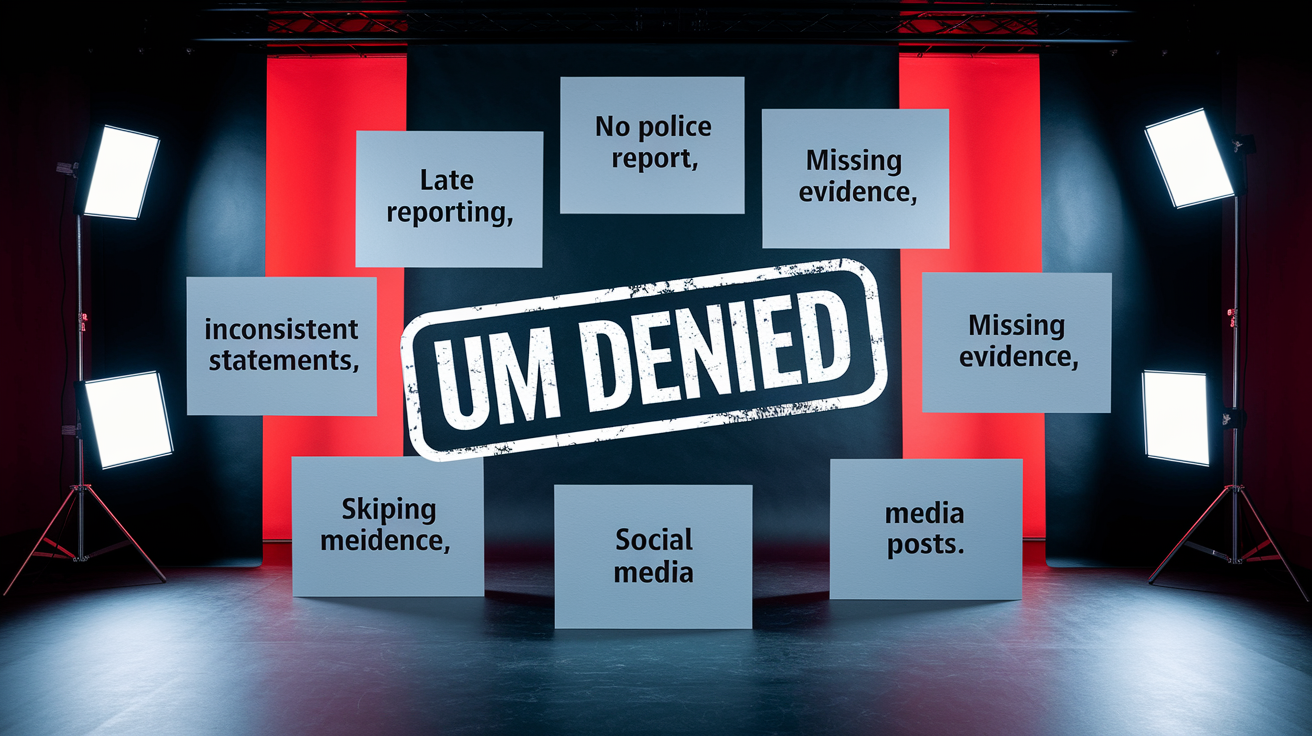

Common Mistakes That Lead to UM Claim Denials

UM hit and run claims get denied more often than standard collision claims because insurers look hard at whether the crash really happened and whether you reported it on time. Small mistakes in the first days can kill an otherwise valid claim. Here are the six most common reasons UM claims fail.

-

Late reporting. Waiting more than 24 to 72 hours to file a police report or notify your insurer without a valid excuse (hospitalization, unconsciousness) gives the insurer grounds to deny. If you missed the deadline, document why (you were in the ER, you didn’t realize the other driver left until later). Some insurers accept reasonable cause, but many don’t.

-

No police report. If you didn’t call the police and file an official report, the insurer has no independent record that a crash occurred. A report filed days later might still help, but timeliness matters.

-

Inconsistent statements. Saying you were hit from the left in your recorded statement but the police report says rear end, or changing details about speed or lane position, tells adjusters you’re being dishonest. Stick to what you know and admit when you’re unsure.

-

Missing evidence. No photos, no witnesses, no medical records, and a vague story make it easy for insurers to conclude the crash didn’t happen or wasn’t serious. Gather everything, even minor details.

-

Skipping medical care or delaying treatment. If you don’t see a doctor until two weeks after the crash, the insurer will say your injuries came from something else. Go the same day or within 24 hours, even for “minor” pain.

-

Social media posts. Posting photos of yourself at the gym, on vacation, or doing physical activities while claiming severe injury gives insurers ammunition to deny or reduce your claim. Assume the adjuster will search your profiles.

If your claim gets denied, the insurer has to send a written explanation. Review it carefully. Many denials rest on procedural errors (late notice, missing forms) that can be appealed if you have a valid reason. Keep every letter, email, and claim document. If the denial feels wrong, consider talking to an attorney who handles UM disputes in your state.

How to Strengthen and Support Your UM Hit‑and‑Run Claim

A well documented claim settles faster and for more money than a thin one. Insurers pay when the evidence is clear and your story holds up under scrutiny. You can improve your claim’s strength at every stage, from the crash scene to final settlement.

First, keep a detailed timeline. Write down every doctor visit, every call to your insurer, every missed day of work. Include dates, times, and brief notes. If your memory’s hazy six months later, this log will fill the gaps.

Second, follow every treatment plan your doctor recommends. If they prescribe physical therapy, go to every session. If they refer you to a specialist, make the appointment. Gaps in treatment let insurers say you weren’t really hurt or that you caused your own延长ed recovery.

Five things that strengthen your UM claim:

- Get independent witness statements in writing. A signed, dated statement from someone who saw the crash or the fleeing vehicle is gold. Even a short paragraph helps.

- Request medical narratives from your treating doctors. Ask your doctor to write a brief report linking your injuries to the crash, explaining your prognosis, and noting any permanent limitations. Insurers trust doctors more than patients.

- Get multiple repair estimates. Two or three estimates from licensed shops show the insurer you’re not inflating damage. If your car’s totaled, get a written appraisal of its pre crash value.

- Keep a daily symptom journal. Note pain levels, activities you couldn’t do, sleep disruptions, mood changes. A month of entries builds a clear picture of how the crash affected your life.

- Review your policy for stacking or additional coverage. If you insure multiple vehicles under the same policy, some states let you stack UM limits (three cars with 25,000 dollars each = 75,000 dollars total). Check your declarations page and ask your insurer if stacking applies.

Don’t accept the first settlement offer if it feels low. Insurers often open with a number below what they’re willing to pay. You can negotiate. If the insurer refuses to move and the offer doesn’t cover your bills and lost wages, you might need arbitration or legal help to push for a fair payout. Document every offer in writing and compare it to your total documented losses before you sign.

Final Words

Act fast: call police, document the scene, get medical care, and notify your insurer right away.

This post walked you through immediate actions, state reporting deadlines, and how uninsured motorist coverage applies. It also covered required documents, what insurers check, common denial mistakes, and ways to strengthen your claim.

Follow the checklist and meet the timelines, that’s how to file an uninsured motorist claim after a hit and run and give your claim the best chance. You’ve got this.

FAQ

Q: What should you not say when making an insurance claim?

A: When making an insurance claim, avoid admitting fault (saying “my fault” or “sorry”), guessing details, downplaying injuries, giving recorded statements without checking, or signing releases before getting estimates.

Q: What percent of hit and run cases get solved?

A: The percent of hit-and-run cases solved varies by state and evidence, but many are solved less often than other crashes—often under half—depending on witness tips, cameras, and police resources.

Q: What is the minimum compensation for a hit and run case?

A: There is no fixed minimum compensation for a hit-and-run; payments depend on your damages, your uninsured motorist limits or other coverages, and state rules—check your policy limits.

Q: Does your insurance go up if you are hit by an uninsured motorist?

A: Your insurance may still rise after being hit by an uninsured driver; because you were not at fault it often shouldn’t, but filing a claim can affect rates—ask your insurer and use UM coverage.