{kind=link}

Think filing a USAA car insurance claim will be a headache?

It doesn’t have to be.

You can start a claim by phone, online, or in the USAA mobile app in minutes.

This post walks you step by step: what to do at the scene, which photos and documents matter, and how USAA handles adjusters, inspections, and repairs.

Read on to learn exactly how to file, what to expect, and the first quick step you can take right now – call USAA at 1-800-531-8722 or open the app.

Immediate Steps to Start Your USAA Claim and Access the Claims Portal

Call 1-800-531-8722 to file your USAA car insurance claim. It’s open 24/7. You can also log into your USAA account and use the claims portal, or file through the mobile app by tapping the claims section. You’ll need your policy number and basic accident details: where it happened, when, and what went down.

At the scene, safety comes first. Then grab evidence before cars get moved or witnesses take off. Snap photos of everything. The whole scene, each vehicle, impact points, debris, traffic signs, road conditions, weather. Get witness names and phone numbers. If police show up, ask for the report number and the officer’s name. Even if you feel fine, consider getting checked out that day. Medical records that start immediately help your claim later.

After filing, USAA gives you a claim confirmation number. Screenshot it or write it down. An adjuster will contact you within 24 to 48 hours to walk you through what’s next, like scheduling an inspection or setting up a repair estimate. Reporting fast keeps things moving and shows you’re cooperating under your policy terms.

Steps to Start Filing Right Now

- Call 911 if anyone’s hurt or the scene isn’t safe.

- Move somewhere safe and turn on your hazard lights.

- Take photos and video of the scene, vehicles, and damage.

- Swap driver and insurance info with everyone involved.

- Grab witness names, numbers, and quick statements if you can.

- Contact USAA at 1-800-531-8722 or file online as soon as possible.

Understanding the USAA Car Insurance Claim Process From Start to Finish

Once you file, USAA assigns an adjuster. This person calls or emails to confirm what happened, asks questions, and explains next steps. Your adjuster handles the investigation, arranges inspections, reviews repair estimates, and approves payouts. They’re your main contact the whole way through.

USAA figures out liability by reviewing your statement, police reports, photos, witness accounts, and sometimes the damage itself. Clear liability means faster processing. Split fault or disputes mean more back and forth, more questions, more documentation. Your adjuster might ask for the same thing twice or request medical records, repair invoices, and signed statements.

After the initial review, USAA schedules a vehicle inspection. You can take your car to a USAA shop, meet an adjuster at home, or upload photos through the app. The adjuster or shop writes an estimate. USAA reviews it, approves it, then either pays the shop directly or cuts you a check. If your car’s totaled, USAA offers actual cash value based on what your vehicle was worth before the crash.

Payout timelines vary. Simple property damage with clear fault often wraps up in one to three weeks. Injury claims take months because treatment continues and full costs aren’t known yet. USAA usually settles property damage first, then handles bodily injury separately.

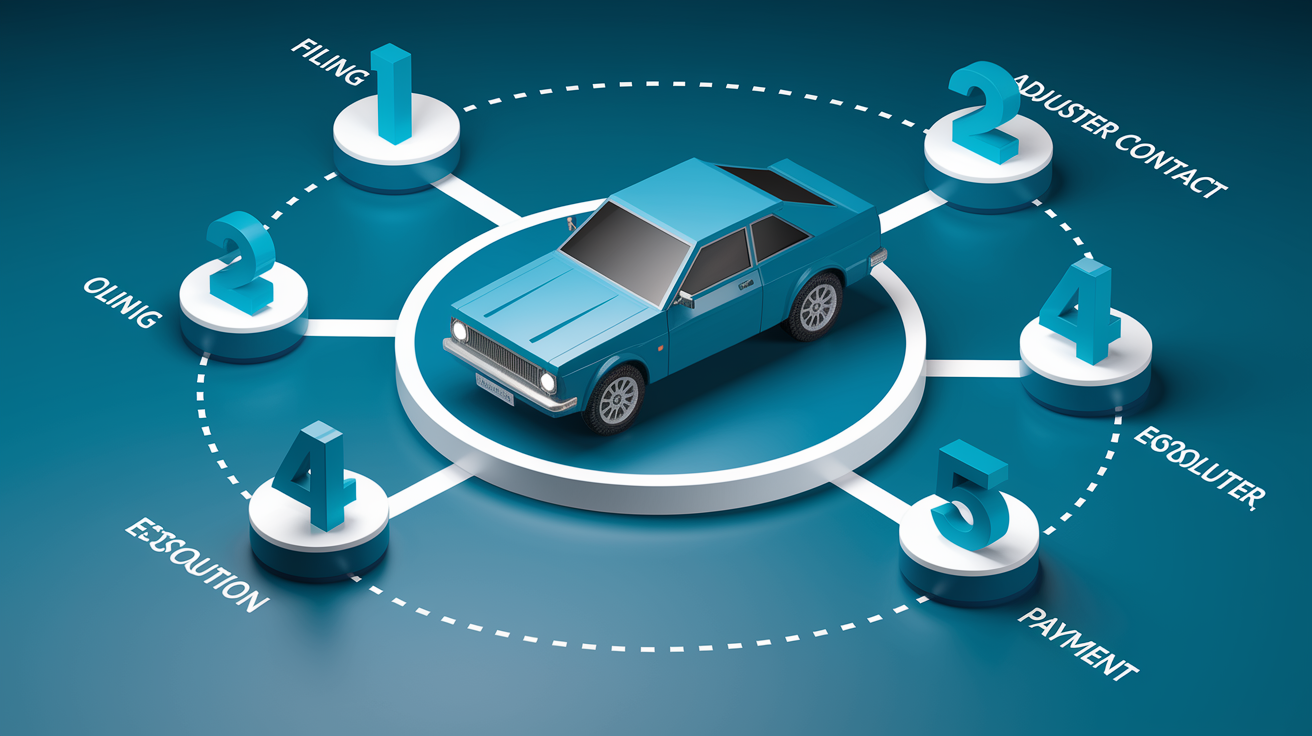

| Stage | What Happens |

|---|---|

| Filing | You submit accident details, get a claim number, and USAA logs your case. |

| Adjuster Contact | An adjuster reaches out within 24–48 hours to confirm details and ask for documents. |

| Inspection | Vehicle gets inspected in person or through photos, damage is assessed, estimate is written. |

| Estimate Approval | USAA reviews and approves the repair estimate or total loss value. |

| Payment | USAA sends payment to the shop, lienholder, or you, minus your deductible if it applies. |

Required Documents and Evidence to File Your USAA Claim Successfully

Complete documentation keeps your claim moving and cuts down on delays or disputes. USAA adjusters need enough info to verify the accident, confirm coverage, assess damage, and approve payment. Missing documents trigger requests for resubmissions or extra proof.

USAA asks for a lot before finalizing payments. Gather everything below and keep digital and physical copies somewhere you can grab them anytime. Phone, folder, cloud drive, whatever works.

- Photos and video of the entire scene, all vehicles, damage zones, debris, skid marks, traffic controls, weather

- Witness names, phone numbers, addresses, written or recorded statements if you got them

- Police report number, officer’s name, the agency that filed it

- Your driver’s license number and a photo of your license

- Proof you own the vehicle: registration or title

- Repair estimates from body shops or mechanics

- Medical records, treatment notes, hospital bills, prescription receipts if anyone was injured

- A log documenting symptoms, pain, missed work, daily limitations from injuries

- Lost wage records: pay stubs, employer letters, W-2s

- Claim confirmation number from USAA

- Notes from every call, email, or conversation with adjusters, including dates, names, what was said

- Signed documents related to repairs, towing, or rental vehicles

Filing a USAA Claim Through the Mobile App, Online Portal, or Phone

The online portal lets you enter accident details, upload photos and documents, track your claim, and get your confirmation number instantly. It’s open 24/7 and works well if you have everything ready and prefer entering data yourself.

The mobile app does the same thing with added convenience. File, upload photos straight from your camera roll, check claim updates in real time. It’s efficient for straightforward claims where you don’t need live help and want everything handled from one device.

Phone filing at 1-800-531-8722 is often better for complex accidents, multi-vehicle crashes, injuries, or situations where you need guidance right away. A live rep walks you through it, answers questions on the spot, and can flag issues or missing details before they slow you down later. Phone filing works after hours and weekends, same as the online options.

- Online portal: best when you want control, prefer entering data at your own speed, uploading documents in bulk

- Mobile app: fastest for on-the-go filing, photo uploads straight from the scene, real-time claim tracking

- Phone: ideal for urgent help, complex cases, questions during filing, when you want a human confirming next steps immediately

- All three methods: available 24/7, nights, weekends, holidays

What to Expect From USAA Adjusters, Inspections, and Vehicle Repair Options

After filing, your adjuster handles the inspection and repair process. USAA may send a field adjuster to your home, ask you to bring the car to a USAA shop, or let you submit detailed photos through the app. Once damage is assessed, the adjuster writes or reviews an estimate and approves the work.

USAA often recommends preferred repair shops in their direct repair network. These shops have agreements with USAA that can speed up approvals, streamline payments, sometimes offer guarantees on the work. Using a preferred shop usually means faster turnaround. But you’re not required to use one. You can choose any licensed facility.

Before signing repair agreements, read every page. Some documents include language that affects your control over the claim. If a shop asks you to sign broadly worded forms, ask what you’re agreeing to and whether USAA requires it.

Understanding Assignment of Benefits (AOB)

An Assignment of Benefits is a legal document that lets a third party, like a repair shop, step in and seek payment directly from your insurer. You sign an AOB, drop off your vehicle, and the shop handles all payment communication with USAA.

AOBs can speed up repairs because the vendor takes over the claim process. But they also shift control. Once you sign, the vendor becomes the policy beneficiary, not you. You may lose transparency into negotiations, payment amounts, dispute resolution. If work stalls, scope is disputed, or fraud is suspected, USAA’s ability to help you may be limited because the vendor now holds the claim rights.

In some states, AOBs are linked to increased litigation and fraud. The long-term effect can mean higher premiums and worse claims experiences across the board. Read AOB clauses carefully. Ask whether signing is truly required or just preferred. If you’re unsure, consult a lawyer or your own insurance agent before signing.

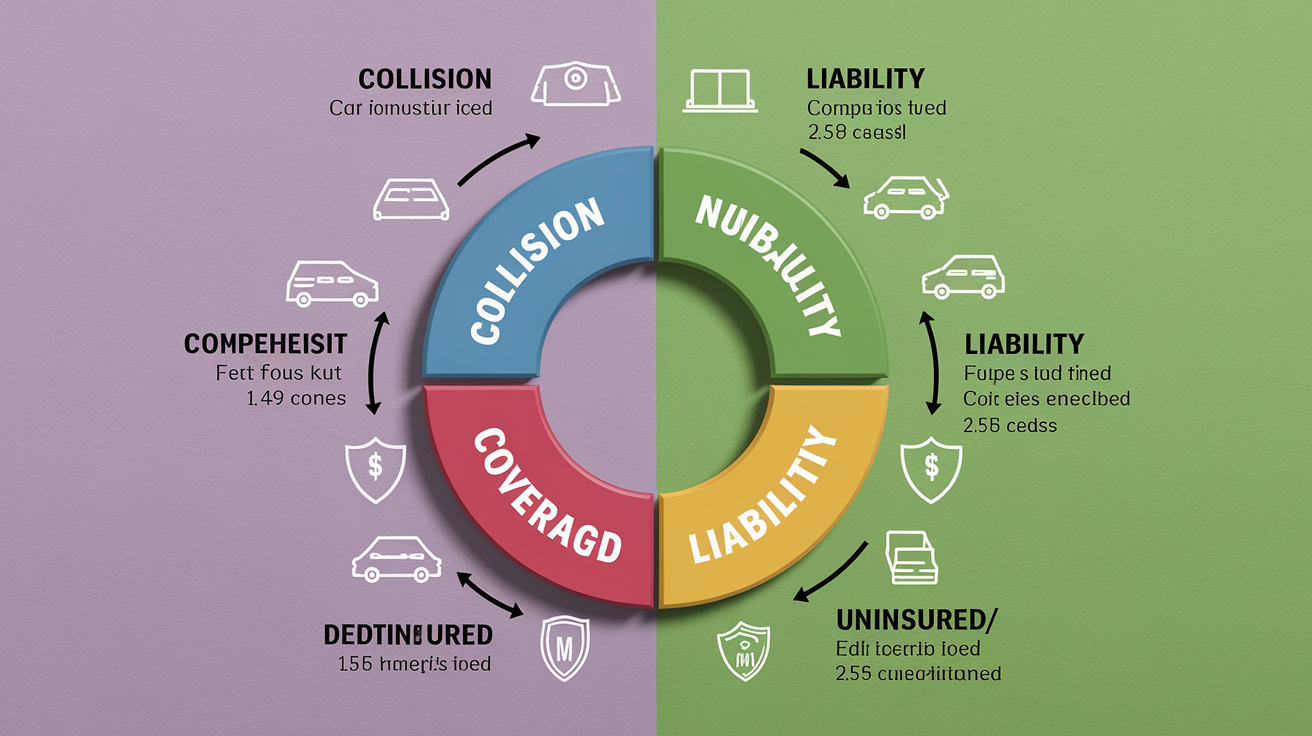

Deductibles, Coverage Types, and How They Affect Your USAA Claim

Your deductible is what you pay out of pocket before USAA covers the rest. If you’ve got a 500 dollar collision deductible and repairs cost 3,200 dollars, you pay 500 and USAA pays 2,700. Deductibles apply per incident and vary by coverage type. Collision, comprehensive, sometimes uninsured motorist coverage each have separate deductibles.

Coverage type determines what USAA will pay and under what circumstances. Collision covers damage from a crash with another vehicle or object. Comprehensive covers non-crash events like theft, hail, vandalism, hitting an animal. Liability covers damage or injuries you cause to others, but it doesn’t pay for your own vehicle or injuries. Uninsured and underinsured motorist coverage steps in when the at-fault driver has no insurance or not enough to cover your losses.

Policy limits cap how much USAA will pay per accident. If your property damage liability limit is 25,000 dollars and you cause 40,000 dollars in damage to another vehicle, USAA pays up to 25,000 and you’re responsible for the remaining 15,000. Understanding your limits and coverage types before filing helps you know what to expect and whether you’ll face out-of-pocket costs.

| Coverage Type | Impact on Claim |

|---|---|

| Collision | Pays for damage to your vehicle after a crash, your deductible applies, USAA pays repair or actual cash value. |

| Comprehensive | Covers non-crash damage like theft, hail, vandalism, glass. Separate deductible, often faster to process than collision. |

| Liability | Covers damage or injuries you cause to others, no deductible, doesn’t pay for your vehicle or your injuries. |

| Uninsured/Underinsured Motorist | Pays when at-fault driver has no insurance or insufficient coverage, may have a deductible, requires proof the other driver is uninsured or underinsured. |

Specialty Claim Types: Total Loss, Glass Damage, Theft, Hail, and More

A total loss happens when repair costs exceed your vehicle’s actual cash value or the damage is so severe the car isn’t safe to repair. USAA figures out actual cash value by looking at your car’s make, model, year, mileage, condition before the accident, and local market prices for similar vehicles. If your car’s totaled, USAA pays actual cash value minus your deductible. If you owe more on your loan than the payout, gap insurance covers the difference, assuming you have it.

Glass claims, like a cracked windshield from a rock, often fall under comprehensive. Some USAA policies include a lower or zero deductible for glass-only repairs. Windshield replacement usually requires an estimate from a glass shop, photos of the damage, confirmation the crack isn’t related to a collision.

Theft and vandalism claims also fall under comprehensive. If your car gets stolen, file a police report immediately and give USAA the report number, photos of where the vehicle was last parked, proof of ownership. USAA typically waits a set period, often 30 days, before paying a total loss settlement in case the vehicle’s recovered. Vandalism claims need photos of the damage, a police report, sometimes witness statements.

- Total loss: actual cash value payout based on pre-accident condition, minus deductible, lienholder paid first if you have a loan

- Glass and windshield: covered under comprehensive, may have reduced or zero deductible, fast turnaround if damage is clear

- Theft: police report required, 30 day waiting period common, proof of ownership and last known location needed

- Hail and storm damage: photos of dents, broken glass, body damage required, claims often spike after severe weather, USAA may send field adjusters to affected areas

- Animal collision: hitting a deer or other animal is comprehensive, police report helpful but not always required, photo documentation of damage and scene speeds approval

- Vandalism: police report, photos, witness information, USAA may investigate if damage appears suspicious or fraud is suspected

Rental Car Reimbursement and Towing Coverage When Filing With USAA

Rental reimbursement coverage pays for a rental car while your vehicle’s being repaired or after a total loss until you get your settlement. USAA sets daily and total limits. Common examples are 30 dollars per day up to 900 dollars total, or 40 dollars per day for 30 days. Check your policy declarations page to see your exact limits.

Towing and roadside assistance coverage reimburses the cost of towing your car to a repair shop or your home after an accident or breakdown. Limits vary by policy, often 75 to 100 dollars per tow. If you use a tow service at the scene, keep the receipt and submit it to USAA for reimbursement. Some USAA policies include roadside assistance that arranges towing directly without you paying upfront.

- Rental reimbursement applies only while your car’s undrivable due to a covered claim, not for routine maintenance or elective repairs.

- Rental limits are per day and per claim. Once you hit the total, you pay any additional days yourself.

- USAA may direct bill rental agencies in their network so you don’t pay upfront, but you can also rent elsewhere and submit receipts for reimbursement.

- Towing coverage requires a receipt showing the date, tow distance or flat fee, destination. Submit through the app, portal, or mail a copy.

Why USAA May Deny a Claim and How to Respond

USAA may deny a claim if the damage isn’t covered under your policy, if you missed a required step like filing a police report, if the accident happened while you were using your vehicle for excluded purposes like commercial delivery, or if USAA determines you misrepresented facts during the claims process. Other common reasons include lapsed coverage at the time of the accident, failure to cooperate with the investigation, or suspicion of fraud.

When USAA denies a claim, they send a denial letter explaining the reason and citing the specific policy language. Read it carefully. If the denial’s based on missing documentation or a misunderstanding, you can often fix it by submitting the correct information or clarifying the facts.

- Request a written explanation if the denial letter is unclear or doesn’t reference specific policy sections.

- Gather any missing documents or evidence that supports your side: photos, witness statements, repair estimates, police reports, medical records.

- Call your USAA adjuster to discuss the denial and ask what additional information might change the decision.

- Escalate to a supervisor if you think the denial is incorrect or the adjuster’s unresponsive. Ask for the supervisor’s name and contact information.

- File a formal appeal by submitting a letter with your claim number, a clear explanation of why the denial is wrong, and copies of supporting documents. Send it to the address listed in the denial letter or through your online account.

Final Words

Start by filing the claim as soon as it’s safe: use the USAA app, the online portal, or call 1-800-531-8722. Have your policy number, photos, and the police report number ready.

Expect an adjuster, an inspection, and steps for repair, rental, or payout. Know your deductible and keep copies of every message or receipt.

If you need to usaa car insurance file a claim, start now, keep clear records, and ask questions along the way. You’ll get this sorted.

FAQ

Q: How to file a claim with USAA insurance?

A: Filing a claim with USAA means reporting the loss via the USAA mobile app, the online claims portal, or by calling 1-800-531-8722; have your policy number, accident details, and photos ready.

Q: How long do you have to file an auto insurance claim with USAA?

A: The time to file an auto claim with USAA is as soon as possible—ideally within 24 hours; report promptly to preserve evidence and avoid coverage or investigation issues.

Q: What number is 1 800 841 3000? / What is the 800 number for USAA claims?

A: The number 1-800-841-3000 is not the USAA claims line; the USAA claims phone number is 1-800-531-8722. Use that, the app, or the online portal to report claims 24/7.