{kind=link}

Filing a claim can end up costing you more than the repair itself.

Sounds crazy, but at-fault collision claims often raise your rate 20% to 40% for three to five years.

That means a small repair might lead to hundreds extra per year.

But sometimes filing still saves money.

This post shows the six things that matter—deductible, repair estimate, expected premium increase, years the hike lasts, vehicle value, and past claims.

I’ll give a simple break-even formula and clear steps so you can pick the smarter money move.

Key Cost Comparison Factors When Choosing Between a Collision Claim and Paying Out of Pocket

Your deductible controls what you pay right now, but premium increases control what you’ll pay for the next three to five years. That’s the part most people miss.

Most collision deductibles sit somewhere between $250 and $1,000. File a claim and you pay that deductible immediately. The insurer covers the rest. Pay out of pocket and you’re covering the entire repair yourself. But the difference between those two numbers is only half the story. What really matters is whether the money you save today gets wiped out by higher premiums down the road.

At-fault collision claims typically bump your annual premium by 20% to 40%. For a lot of drivers, that’s $300 to $800 extra per year. And it sticks around. Usually three to five years. So if you’re paying $1,200 a year and your premium goes up $300 for three years, you’re looking at $900 in extra costs. Whether that matters depends on whether your repair is $800 or $4,000, whether your deductible is $500 or $1,000, and whether your insurer will forgive your first accident.

You need an accurate repair estimate before you can run any of this math. A bumper repair might cost $800 to $1,800. Fender or door panel work can run $800 to $2,500. Moderate front-end damage often lands between $2,500 and $7,000. Let’s say your repair is $2,500 and your deductible is $500. Filing saves you $2,000 upfront. But if your premium goes up $300 per year for three years, that’s $900 in extra premiums. Your net benefit is $2,000 minus $900, so $1,100 in your favor. That’s the kind of comparison you’re trying to make every single time.

When you’re deciding between a collision claim and paying out of pocket, these six variables matter most:

- Deductible amount – Higher deductibles mean less upfront benefit from filing.

- Repair estimate – The higher the cost, the more filing helps offset future increases.

- Annual premium increase – A $200 bump versus a $700 bump completely changes the break-even point.

- How many years the increase lasts – Three years versus five can double or triple your total extra premium.

- Vehicle value – For older cars with low market value, even big repairs might not justify a claim that stays on your record.

- Prior claim history – If you’ve filed recently, another claim could trigger much bigger rate hikes or nonrenewal.

Understanding Collision Deductibles and Their Impact on the Claim Decision

If your repair cost is less than or equal to your deductible, filing a collision claim gives you zero financial benefit. You’re paying the full cost either way.

This is where people get stuck. A $400 scratch with a $500 deductible means you’re paying $400 whether you file or not. The claim just adds a record that could raise your premiums later. On the flip side, if the repair is $2,500 and your deductible is $500, the insurer would pay $2,000 if you file. That $2,000 has to be weighed against the multi-year premium increases that follow.

The size of your deductible changes everything. A $250 deductible makes filing worth it for smaller repairs because you’re only out $250 upfront. A $1,000 deductible means the repair has to be way bigger before the immediate savings outweigh the long-term premium hit.

| Deductible Amount | When It Favors Paying Out of Pocket | When It Favors Filing a Claim |

|---|---|---|

| $250 | Repair costs below $1,500 with expected premium increases of $400+/year | Repair costs above $2,000 or injuries involved |

| $500 | Repair costs below $2,000 and expected premium increases of $300+/year for 3 years | Repair costs above $2,500 or structural damage |

| $1,000 | Repair costs below $2,500 with expected premium increases of $500+/year | Repair costs above $3,500 or total loss scenarios |

| $1,500 | Repair costs below $3,000 with premium increases expected over multiple years | Repair costs above $5,000 or major front-end/frame repairs |

How Filing a Collision Claim Affects Your Insurance Premiums Long Term

When you file an at-fault collision claim, insurers recalculate your risk profile. They usually increase your base rate, remove claim-free discounts, or both. The typical premium jump ranges from 10% to 50% of your prior annual premium. For most drivers, that’s an extra $200 to $1,200 per year. The exact number depends on your insurer’s underwriting rules, your state’s rating regulations, and how clean your record was before the accident. A first-time claim by someone with 10 years of clean history might see a smaller bump than a second or third claim in a short window.

That premium increase doesn’t disappear after one year. Most insurers apply these adjustments for three to five years. They review your claims history at every renewal and when you shop for new quotes. If your premium goes up $400 per year and stays elevated for four years, you’re paying an extra $1,600 total. That’s on top of the deductible you already paid. This is why a $1,000 repair can end up costing you $2,000 or more when you file a claim, even though your deductible was only $500.

Accident forgiveness can completely change the outcome if your policy includes it. With accident forgiveness, your first at-fault claim may not raise your premium at all. If you have this coverage and your repair estimate is $3,000, filing the claim costs you only the deductible because there’s no rate penalty. But if you already filed a claim two years ago and you’re considering a second one, your insurer may treat the new claim way more harshly. Some policies explicitly say a second claim removes accident forgiveness and triggers steeper rate increases or even nonrenewal.

Here are the five big factors that determine how much your rate will increase after a collision claim:

- Fault determination – At-fault claims almost always raise rates. Not-at-fault or subrogated claims often don’t.

- Claim frequency – Your second or third claim in a few years triggers bigger increases.

- State rules – Some states cap how much insurers can raise rates after one accident or mandate lookback periods.

- Insurer underwriting formulas – Each company weighs claims differently. One might add $300/year, another $700/year for the same accident.

- Discount removal versus base rate increase – Losing a 20% claim-free discount can hurt as much as a direct rate hike.

Repair Cost Examples and Damage Thresholds That Influence Filing vs Paying Out of Pocket

The type of damage dictates the repair cost, and the repair cost determines whether a claim makes financial sense.

Minor cosmetic repairs like a dent in a door or a scratched bumper often run $400 to $1,500. Moderate damage involving multiple body panels, paint work, or sensor recalibration typically falls in the $1,500 to $4,000 range. Structural repairs to the frame, major front-end collisions, or damage involving safety systems can easily climb above $5,000.

An $800 repair with a $500 deductible might save you $300 immediately if you claim, but if your premium goes up $350 per year for three years, you’ll pay $1,050 in extra premiums. Paying the $800 yourself saves you $250 overall.

At the other end, a $4,000 repair with a $1,000 deductible saves you $3,000 upfront. If your annual premium increase is $400 and lasts four years, that’s $1,600 in extra premiums. Your total claim cost is $1,000 deductible plus $1,600 in premiums, which equals $2,600. Paying $4,000 out of pocket would cost you $1,400 more than filing the claim, so the claim clearly wins.

Common accident damage breaks down like this:

- Cosmetic – scratches, small dents, bumper scuffs ($300 to $1,500)

- Moderate – crumpled fenders, door panel replacement, headlight assemblies ($1,500 to $4,000)

- Structural – frame damage, suspension, axle repairs ($4,000 to $10,000+)

- Electronic/sensor – cameras, radar, airbag systems, often bundled with other repairs ($500 to $3,000 added cost)

| Damage Type | Estimated Repair Range | Typical Filing vs OOP Recommendation |

|---|---|---|

| Cosmetic (bumper, scratch, minor dent) | $400 to $1,500 | Usually pay out of pocket unless deductible is very low ($250) and premium increase is minimal |

| Moderate (panels, paint, multiple parts) | $1,500 to $4,000 | Run the break-even formula. Decision depends on deductible and expected premium increase |

| Structural or major front-end | $5,000+ | Usually file a claim unless vehicle value is very low or you have multiple prior claims |

Break-Even Math for Collision Claims: When a Claim Saves Money vs When Out of Pocket Wins

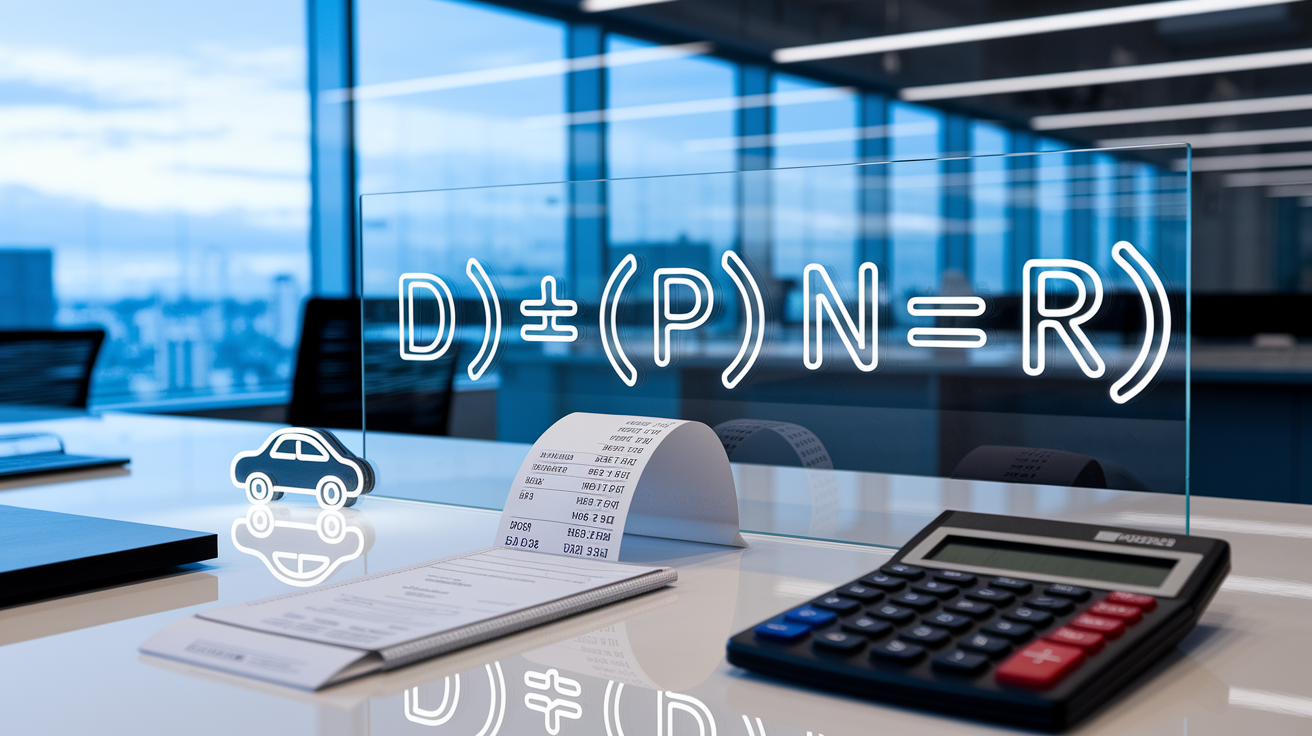

The break-even formula is straightforward. File a claim if your deductible plus the total premium increases over the next few years is less than the full repair cost.

In shorthand, that’s D + (ΔP × N) < R, where D is your deductible, ΔP is the annual premium increase, N is the number of years the increase lasts, and R is the repair cost. If the left side of that equation is smaller than R, filing a claim saves you money. If it’s bigger, paying out of pocket is cheaper.

Multi-year premium effects are what most people underestimate. A $300 per year increase sounds manageable until you realize it’s $300 every year for three or four years. That’s $900 to $1,200 in total extra premiums. If your deductible is $500 and your repair is $2,500, you’re comparing $500 plus $900 (claim cost of $1,400) against paying $2,500 yourself. The claim saves you $1,100. But if the repair is only $1,200 and your deductible is $1,000 with a $200 annual increase over three years, you’d pay $1,000 plus $600, which totals $1,600. Paying the $1,200 yourself saves you $400.

High deductibles shift the equation heavily toward paying out of pocket for smaller claims. Multiple prior claims make future premium increases steeper, which also tips the balance away from filing. If you’ve already filed one claim this year and you’re deciding on a second, ask your insurer for a specific estimate of how much a second claim would raise your premium. The increase for a second claim is usually way larger than for a first.

Here’s how to run the break-even calculation step by step:

- Get a written repair estimate (R) from at least one shop.

- Check your policy documents or call your agent to confirm your deductible (D).

- Ask your insurer to estimate the likely annual premium increase (ΔP) and how many years (N) it will last.

- Multiply ΔP by N to get the total premium cost over the affected period.

- Compare D + (ΔP × N) to R. If the sum is less than R, file the claim. If the sum is more than R, pay out of pocket.

Special Situations That Change Whether a Collision Claim or OOP Payment Makes Sense

When repair costs approach or exceed your vehicle’s actual cash value, insurers often declare a total loss. The typical threshold is around 70% to 75% of the car’s market value, though this varies by company and state.

If your car is worth $4,000 and the repair estimate is $3,200, the insurer might total it and pay you the $4,000 value minus your deductible. In that case, you’re not really choosing between claim and out-of-pocket repair anymore. You’re deciding whether to accept the total-loss settlement or keep the car with a salvage title. Salvage titles usually reduce a vehicle’s resale value by 20% to 40%, so even if you repair it yourself, you’ll take a hit when you eventually sell or trade it.

Diminished value is another layer. If another driver is at fault and their insurer accepts liability, you may be able to recover diminished value on top of the repair cost. This applies when your vehicle’s market value drops because it now has an accident history, even after perfect repairs. Amounts vary widely and depend on the car’s age, mileage, and the severity of the accident, but recoveries of several hundred to a few thousand dollars are possible in some states. If you file through your own collision coverage because the other driver is uninsured or disputes fault, you usually can’t collect diminished value from your own insurer. You’d need to pursue the at-fault driver directly in small claims or through a lawyer.

Uninsured and underinsured motorist property damage coverage can blur the lines. If the at-fault driver has no insurance, you might file under your uninsured motorist coverage, which sometimes includes a separate deductible or no deductible at all. Check your policy.

Rental car coverage and towing reimbursement also matter. If your policy includes rental reimbursement and you’ll need a rental for a week at $50 per day, that’s $350. Towing and storage fees can add another $100 to $500. When you add those costs to the repair bill, paying out of pocket might mean covering $3,000 instead of $2,500. That shifts the break-even point. If you file a claim, rental and towing are often covered under your policy limits.

Immediate Post-Accident Steps That Affect Your Claim vs Out-of-Pocket Choice

What you do in the first few hours after an accident directly impacts the quality of information you’ll have when deciding whether to file a claim.

Take photos of all vehicle damage, the accident scene, license plates, and any visible road conditions or traffic signs. If the other driver is involved, photograph their insurance card and driver’s license. A police report establishes an official record of fault, weather, road conditions, and witness statements. Many insurers require a police report for claims, and it can help with subrogation if the other driver’s insurer eventually accepts liability. Without a police report, disputes about fault become harder to resolve.

Get at least one written repair estimate before you call your insurer. Some shops offer free estimates. The estimate gives you the repair cost (R) you need for the break-even formula.

Hidden damage is common, especially in front-end collisions where frame or suspension components may be bent but not visible. The initial estimate might say $1,800, but once the shop starts disassembly they find another $1,200 in damage. If you’ve already decided to pay out of pocket and the cost doubles, you can still file a claim as long as you do it within your policy’s reporting window, which is often 30 to 60 days.

Key documentation to gather right after an accident includes:

- Photos of all damage – your vehicle, other vehicles, scene context, road conditions

- Police report – file one even for minor accidents. It helps establish fault and timeline

- Written repair estimates – get one or two. Use them to compare claim cost versus out-of-pocket cost

- Insurer notification – most policies require “prompt” notice of an accident, even if you don’t file a claim immediately. Calling within a day or two protects your coverage if hidden damage emerges later

Practical Tips for Paying Out of Pocket Without Overpaying

When you decide to pay for repairs yourself, you have more control over the shop, the parts, and the timeline.

Some independent shops offer payment plans or discounts for cash payment. Dealerships typically charge more but use OEM (original equipment manufacturer) parts and follow factory repair procedures. Independent shops may use aftermarket or recycled parts, which can cut costs by 20% to 50% but may affect resale value or warranty coverage. Ask the shop to break down labor, parts, and paint separately so you understand where the money goes.

Cosmetic repairs are often negotiable. Paintless dent repair can fix door dings and hail damage for $300 to $600 without repainting, which is way cheaper than traditional bodywork. If your car is older and resale value isn’t a priority, you might skip cosmetic work entirely and only fix functional or safety issues like lights, latches, or structural damage.

Keep all repair receipts and invoices. If you later discover the shop missed hidden damage or if the repair fails, the documentation supports a warranty claim or follow-up work. Some shops offer limited warranties on labor and parts, typically 90 days to one year.

When paying out of pocket, consider these four strategies to avoid overpaying:

- Negotiate repair price – ask for itemized estimates from two or three shops and use them to negotiate. Some shops will match or beat competitors

- Check OEM versus aftermarket parts – aftermarket parts can be 30% to 60% cheaper. Ask about quality, fit, and warranty differences

- Review warranty terms – confirm what’s covered if the repair fails or new issues appear within 30, 60, or 90 days

- Payment plan options – some shops offer financing or installment plans. Compare interest rates to a credit card or personal loan if needed

Sample Scenarios Comparing Collision Claims vs Out-of-Pocket Payment

Real-world examples make the math concrete.

Scenario A: you back into a pole and crack your rear bumper. Repair estimate is $800. Your deductible is $500 and your current annual premium is $1,100. Your insurer estimates a 30% increase if you file, which equals $330 per year for three years, or $990 total. Filing the claim costs you $500 deductible plus $990 in extra premiums, which totals $1,490. Paying $800 out of pocket saves you $690. In this case, pay out of pocket.

Scenario B: you’re in a parking-lot fender-bender where you’re at fault. Damage includes a crumpled fender, broken headlight, and scratched door. Repair estimate is $2,500. Your deductible is $500, and the insurer projects a $300 per year premium increase for three years. Filing costs you $500 plus $900 in premiums, totaling $1,400. Paying $2,500 yourself costs $1,100 more than filing. Here, file the claim and save $1,100.

Scenario C: you slide on ice and hit a guardrail. Repair estimate is $4,000 for front-end work. Your deductible is $1,000 and your insurer says the premium will go up $400 per year for four years. Claim cost is $1,000 plus $1,600, which equals $2,600. Paying $4,000 out of pocket costs $1,400 more. File the claim.

Scenario D: minor cosmetic scratch on a door after a shopping-cart bump. Estimate is $600. Deductible is $500. Even if premium increases are zero, filing saves you only $100 and puts a claim on your record. Pay the $600 yourself.

| Scenario | OOP Cost | Claim Cost (Deductible + Premium Increases) | Better Option |

|---|---|---|---|

| Minor bumper crack, $800 repair, $500 deductible, $330/year × 3 years | $800 | $500 + $990 = $1,490 | Pay out of pocket (saves $690) |

| Fender/headlight damage, $2,500 repair, $500 deductible, $300/year × 3 years | $2,500 | $500 + $900 = $1,400 | File claim (saves $1,100) |

| Front-end collision, $4,000 repair, $1,000 deductible, $400/year × 4 years | $4,000 | $1,000 + $1,600 = $2,600 | File claim (saves $1,400) |

| Cosmetic door scratch, $600 repair, $500 deductible, minimal premium effect | $600 | $500 + possible premium increases | Pay out of pocket (avoids claim record for minimal savings) |

Final Words

If you’re staring at repair estimates and your deductible, focus on the immediate costs and the likely premium bump over 3–5 years. Deductible size affects what you pay today; rate increases affect what you pay later.

Use the break-even formula (D + (ΔP × N) < R), get written estimates, take photos, and watch for special cases like total loss or uninsured drivers. Ask about payment plans and parts choices.

For collision claim vs pay out of pocket after an accident, compare the full math and pick the option that protects your wallet and keeps you covered.

FAQ

Q: Is it better to file a car insurance claim or pay out of pocket? When should I file and when should I pay out of pocket?

A: The decision whether to file a car insurance claim or pay out of pocket depends on repair cost versus your deductible plus expected premium increases over several years; often skip claims under about $1,000–$2,000.

Q: Should you report $10,000 worth of car repair to your insurance or pay out of pocket?

A: You should report $10,000 worth of car repair to your insurance when the repair exceeds your deductible plus expected premium increases; with common deductibles, filing usually makes financial sense for $10,000 repairs.

Q: What not to say to the insurance adjuster?

A: You should not say you were at fault, apologize, guess injury severity, admit prior damage, or agree to a recorded statement without checking first; stick to facts and call your agent.